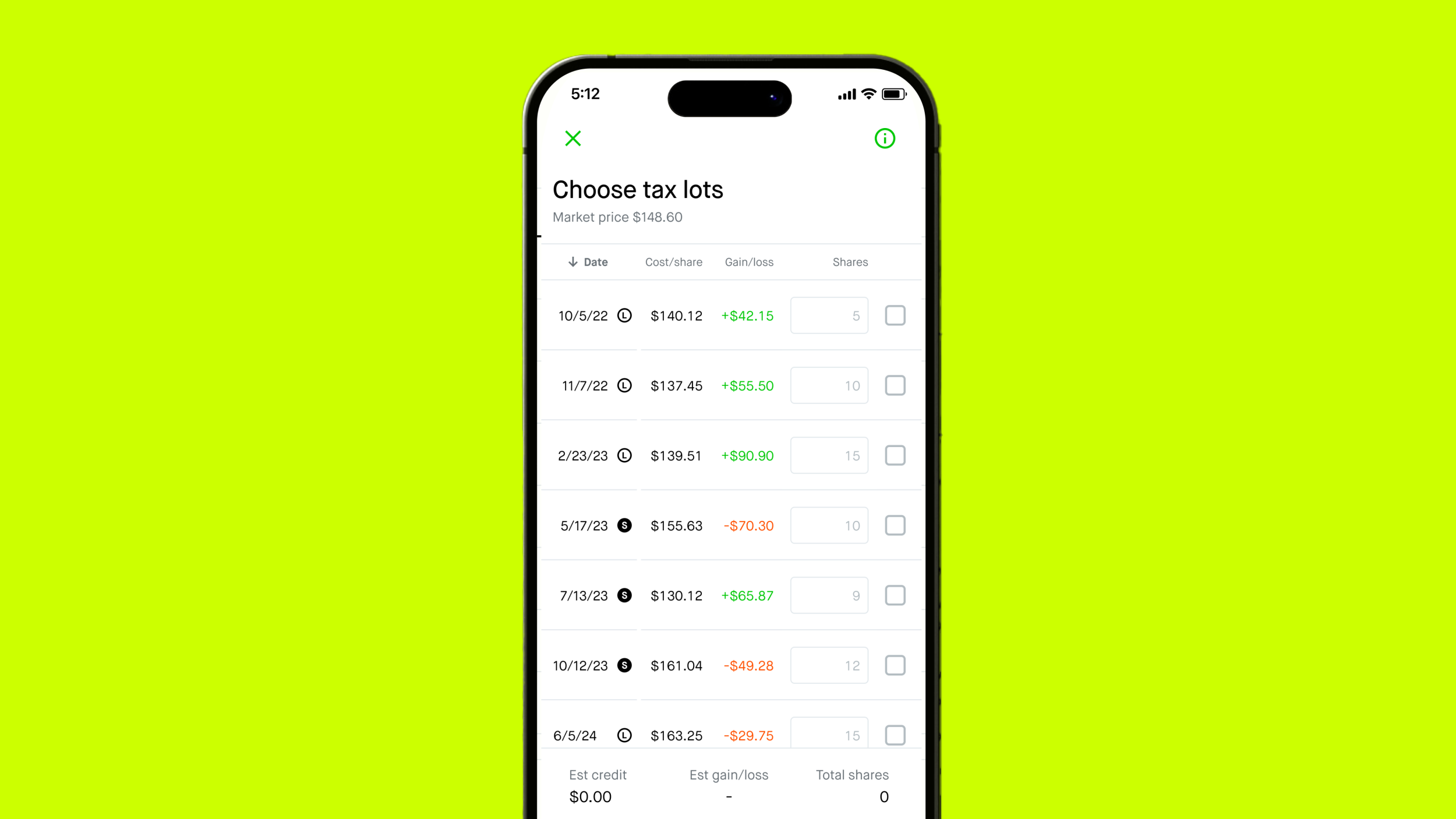

Choosing between FIFO and LIFO for DeFi tax lots in 2026

The 2026 tax landscape for DeFi is defined by the new Form 1099-DA, which requires brokers to report both gross proceeds and cost basis for assets acquired after January 1, 2025. This shift eliminates the ability to ignore on-chain activity, making your cost basis method a primary defense against overpaying taxes on yield farming and liquidity pool rewards.

FIFO (First-In, First-Out) and LIFO (Last-In, First-Out) are the two standard approaches for calculating capital gains. FIFO assumes the oldest tokens in your wallet are the first ones sold or swapped. LIFO assumes the most recently acquired tokens are disposed of first. The choice between these methods doesn't change the total tax you pay over a lifetime of trading, but it significantly impacts your current-year tax liability and cash flow.

Comparison of fifo and lifo choices that change the plan

The table below outlines the core differences in how these methods handle DeFi-specific events like impermanent loss and staking rewards.

| Metric | FIFO | LIFO |

|---|---|---|

| Best for | Long-term holders with low recent activity | High-frequency traders and yield farmers |

| Tax timing | Defers taxes longer if asset prices rise | Accelerates tax liability to current year |

| Complexity | Easier to track across multiple wallets | Requires precise lot matching for every swap |

| Impermanent Loss | Higher reported gains if LP tokens are sold early | Offsets recent gains with recent losses |

When FIFO Works Best

FIFO is generally the safer default for most DeFi participants. It is particularly effective for long-term holders who deposit tokens into liquidity pools and leave them alone. Because you are selling the oldest, lowest-basis tokens first, you defer recognizing gains until those specific lots are finally disposed of. This approach reduces administrative burden, as you only need to track the age of your oldest holdings rather than every single recent transaction.

When LIFO Makes Sense

LIFO is a strategic tool for active yield farmers and high-frequency traders. By selling the most recently acquired tokens first, you can match recent gains with recent losses, potentially lowering your current-year tax bill. This is especially useful in volatile markets where you are constantly rebalancing positions. However, LIFO requires meticulous record-keeping to ensure each swap is correctly attributed to the newest lot, which can be challenging when dealing with fragmented DeFi positions across multiple chains.

Making the Decision

Your choice should depend on your trading frequency and market outlook. If you are holding assets for the long term and expect prices to rise, FIFO helps defer taxes. If you are actively trading and want to minimize current-year liability, LIFO offers more immediate control. Always consult a tax professional to ensure your chosen method is consistently applied and compliant with IRS guidelines for the 2026 tax year.

Where FIFO and LIFO win

Choosing between FIFO (First In, First Out) and LIFO (Last In, First Out) isn't just an accounting preference; it's a strategic lever for your DeFi tax liability. The right lot selection method depends entirely on how you farm yield, how long you hold, and whether your portfolio is trending up or down.

FIFO is the default method the IRS requires if you don't specify otherwise. It matches your oldest assets against your sales first. This method is most effective when you hold assets for the long term. Because it sells the oldest shares first, it often locks in the lowest cost basis, but it also prioritizes long-term capital gains rates if those old assets have been held for more than a year. If you are a buy-and-hold investor who occasionally farms, FIFO provides a predictable, compliant baseline that minimizes administrative overhead.

LIFO sells your most recently acquired assets first. This strategy shines in bear markets or when you are actively trading volatile yield farming positions. By selling the newest, often higher-cost tokens, you can offset current gains with recent losses, reducing your immediate taxable income. However, LIFO requires meticulous record-keeping. Every staking reward, liquidity pool deposit, and airdrop creates a new lot. If your DeFi activity involves frequent swaps and rebalancing, LIFO can significantly lower your tax bill, but only if you can track every single transaction timestamp and price accurately.

The decision often comes down to market direction and activity level. If you are farming in a bull market, FIFO might result in higher taxes because your older, cheaper tokens are sold first. In a bear market, LIFO allows you to harvest recent losses to offset gains. For most DeFi users, the complexity of LIFO is only worth it if you are actively trading. Otherwise, FIFO remains the safer, simpler path to compliance.

Details worth checking

DeFi tax lots require more than just tracking token swaps. You must verify how your specific platform reports data and whether your jurisdiction recognizes impermanent loss as a deductible expense. The following steps outline the critical details that can make or break your 2026 tax filing.

Brokers must report gross proceeds and cost basis for assets acquired after January 1, 2025, under the new Form 1099-DA. Verify that your custodian or exchange provides accurate lot identification, as errors here cascade through your entire return.

Liquidity pool tokens often obscure the underlying cost basis of the contributed assets. Ensure your tax software can split the basis when you withdraw from a pool, or manually calculate the basis reduction to avoid double-treating the principal.

The IRS generally does not allow deductions for impermanent loss unless the position is fully closed and liquidated. Check if your jurisdiction treats this differently, as some regions may allow loss recognition upon pool exit or rebalancing.

Airdrops and governance token rewards are taxable as ordinary income at their fair market value upon receipt. Verify that your tracking tool captures these events, as they are frequently missed in automated DeFi transaction histories.

No comments yet. Be the first to share your thoughts!