DeFi staking has evolved from a niche yield strategy into a staple for savvy investors chasing stable returns amid volatile markets. Yet, as protocols proliferate across chains like Ethereum and Solana, the tax burden of those rewards demands meticulous tracking. IRS Notice 2024-57, released in July 2024, offers brokers a breather from reporting certain DeFi activities on Form 1099-DA, but it places the onus squarely on you, the taxpayer, to capture every DeFi staking rewards tax 2026 event accurately. This transitional relief underscores a harsh reality: unreported income from staking can trigger audits, while precise onchain PnL monitoring ensures compliance without the guesswork.

Over two decades in commodities and DeFi yields have taught me that true value accrues through disciplined oversight, not fleeting trades. Platforms like DefiTaxLots. com exemplify this by delivering real-time onchain PnL staking tracker capabilities, harmonizing FIFO and LIFO methods for tax lots that align with IRS expectations. As 2026 approaches, understanding these dynamics separates the prepared from the penalized.

Decoding IRS Notice 2024-57: Exemptions for DeFi Brokers

This pivotal notice identifies transactions exempt from broker reporting through at least 2026, creating a window where centralized exchanges and DeFi front-ends sidestep 1099-DA obligations. Staking, whether traditional or liquid variants like stETH, falls under this umbrella alongside liquidity provision, lending, and wrapping. Brokers breathe easy, but you cannot. Staking rewards crystallize as ordinary income at fair market value the instant they hit your wallet, per longstanding IRS guidance. Sell those rewards later, and capital gains computations kick in, hinging on your chosen cost basis method.

Exempt DeFi Transactions from 1099-DA Reporting under IRS Notice 2024-57

| Transaction Type | Description/Examples | Broker Reporting | Taxpayer Obligation |

|---|---|---|---|

| Staking transactions (incl. liquid staking and restaking) | Providing digital assets to stake for rewards | Exempt (transitional relief until further guidance) | Report staking rewards as taxable income at fair market value upon receipt; report capital gains/losses on later sale/exchange |

| Liquidity provider transactions | Adding/removing liquidity, minting/burning LP tokens | Exempt (transitional relief until further guidance) | Report any income, gains, or losses from these activities |

| Lending of digital assets | Lending digital assets for interest/yield | Exempt (transitional relief until further guidance) | Report lending interest as income; report gains/losses on repayment or disposal |

| Wrapping and unwrapping digital assets | e.g., Converting ETH to WETH and vice versa | Exempt (transitional relief until further guidance) | Generally non-taxable if 1:1 exchange; track basis for future disposals |

| Short sales of digital assets | Short selling digital assets | Exempt (transitional relief until further guidance) | Report gains/losses upon closing the short position |

| Notional principal contract transactions | e.g., Certain DeFi derivatives or swaps | Exempt (transitional relief until further guidance) | Report income/gains/losses per transaction terms |

Notice the pattern? These exemptions spotlight DeFi's decentralized ethos clashing with regulatory frameworks built for custodians. Extension via Notice 2026-20 pushes relief to year-end 2026, buying time for clearer rules. Yet, this interlude amplifies the need for self-reliant tools. Without broker forms, your DeFi unreported income taxes risk flying under the radar, inviting penalties up to 25% for underreporting.

I've seen investors overlook staking accruals, only to face reconciliation nightmares during tax season. Proactive onchain tracking mitigates this, visualizing inflows against macro trends for a holistic PnL view.

Staking Rewards: Taxable Income You Cannot Ignore

Even as brokers demur, the IRS views staking rewards as compensation for services rendered to the network, taxable upon receipt. Picture depositing ETH into Lido: the stETH you receive carries no basis initially, but subsequent rewards do, valued at then-current prices. Subsequent disposals trigger gain/loss calculations, where FIFO LIFO DeFi tax lots become your strategic lever.

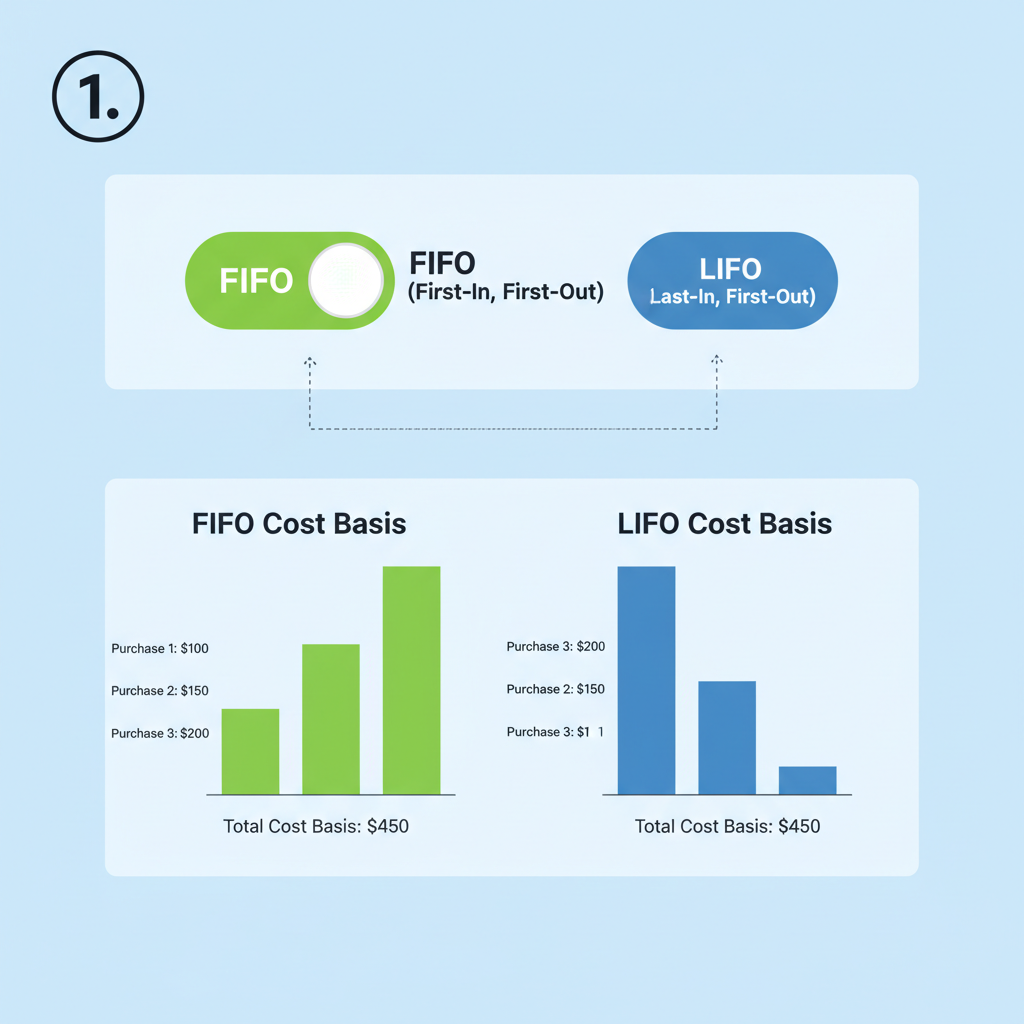

This duality perplexes newcomers. Rewards compound quietly in protocols, often auto-reinvested, blurring income recognition lines. Specialized trackers parse these via wallet imports, attributing basis across lots with FIFO's chronological discipline or LIFO's recency bias. FIFO, the IRS default for digital assets per proposed regs, assumes oldest units sell first, potentially inflating gains in bull markets. LIFO, permissible with adequate records, might shield higher-basis recent acquisitions, curbing short-term liabilities.

Consider a restaker layering EigenLayer atop Lido: multi-hop yields demand granular lot management. Tools excelling here reconcile across chains, flagging IRS Notice 2024-57 DeFi exemptions while computing liabilities. Neglect this, and 2026 filings become a slog.

FIFO vs LIFO: Tailoring Cost Basis for DeFi Tax Efficiency

Cost basis selection shapes your effective rate more than most realize. FIFO mirrors inventory accounting, FIFO suits long-term holders aligning with my mantra that value endures over time. It pairs well with onchain PnL dashboards showing unrealized positions by vintage, revealing macro alignments.

LIFO, conversely, favors active traders front-loading losses from recent high-basis buys. IRS scrutiny intensifies here; records must specify lots pre-transaction, a feat for DeFi's permissionless swaps. Hybrid approaches via specific identification offer precision but burden proof.

In practice, simulate scenarios: FIFO might yield $5,000 gain on a $10,000 ETH stake sale amid rising prices, while LIFO drops it to $2,000 by matching newer lots. Such foresight, rooted in real-time data, fortifies your position as regulations solidify.

Real-time onchain PnL tools bridge this gap, layering tax lot simulations over live positions. DefiTaxLots. com stands out by ingesting wallet data across EVM chains and Solana, auto-classifying staking events per IRS Notice 2024-57 DeFi exemptions. Users toggle FIFO or LIFO effortlessly, previewing 2026 liabilities before filing. This isn't mere accounting; it's strategic intelligence for aligning yields with long-term holdings.

Onchain PnL Tracking: Your Shield Against DeFi Unreported Income Taxes

DeFi's opacity amplifies DeFi unreported income taxes pitfalls. Rewards from protocols like Rocket Pool or Jito often nest within derivatives, evading casual scans. An onchain PnL staking tracker dissects this, timestamping income at block-level precision and assigning basis to lots dynamically. I've advised clients through yield farm cascades where untracked accruals ballooned into six-figure exposures; disciplined monitoring averted that.

Visualize your portfolio's evolution: entry prices plotted against reward epochs, with FIFO projecting conservative gains and LIFO optimizing for volatility. As Notice 2024-57's relief wanes post-2026, such granularity becomes non-negotiable. Platforms reconciling CEX and DeFi flows prevent double-counting, a common snare in hybrid strategies.

FIFO vs LIFO vs Specific ID Example for ETH Staking Rewards Sale

| Method | Cost Basis for 1 ETH Sold (Source) | Sale Price (Dec 2025) | Capital Gain |

|---|---|---|---|

| FIFO | $2,500 (Jan 2025 buy) | $4,000 | $1,500 |

| LIFO | $3,500 (Mar 2025 staking reward) | $4,000 | $500 |

| Specific ID | $3,700 (elected lot) | $4,000 | $300 |

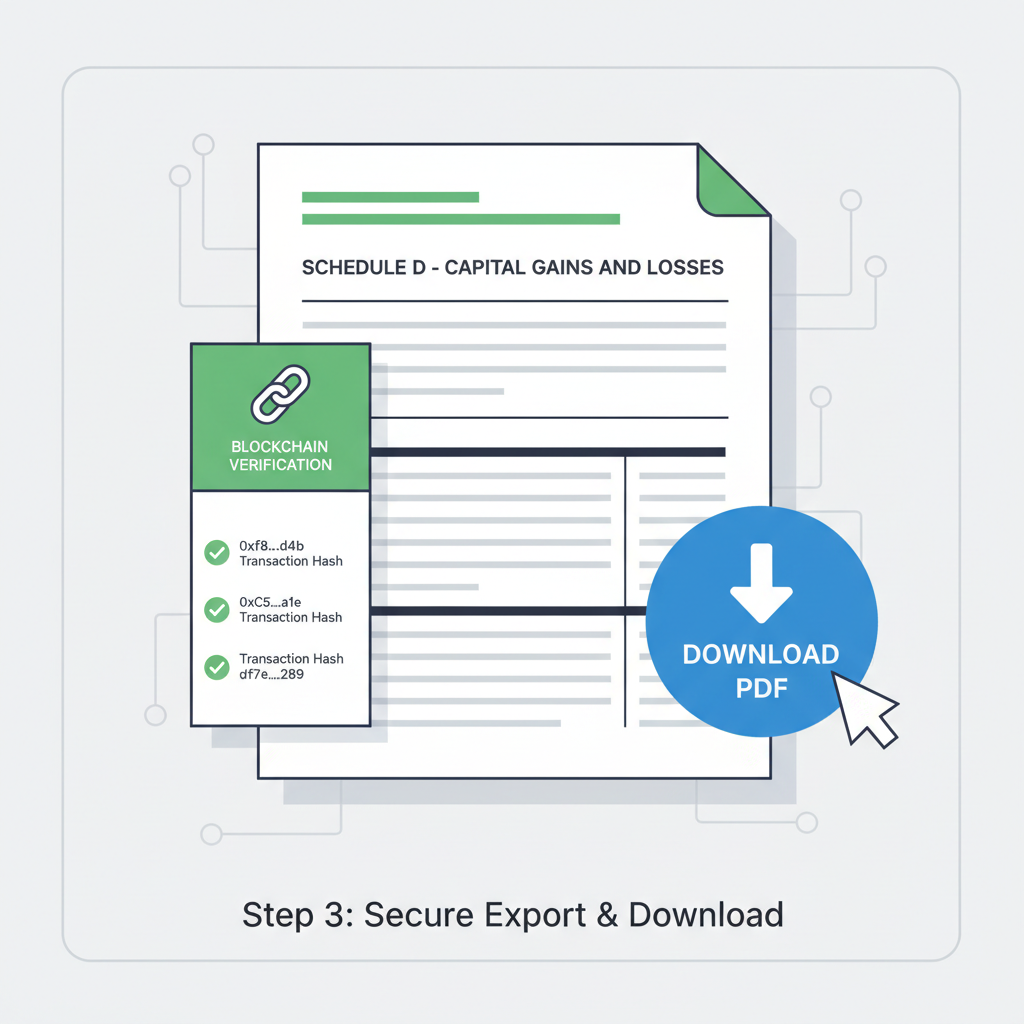

This table illustrates the leverage: LIFO pares taxable events by prioritizing recent, higher-basis rewards. Yet, election rules demand pre-sale specificity, logged irrevocably. DeFi's speed tests this; onchain trackers automate compliance logs, timestamped for audit defense.

Navigating 2026 Filings: Best Practices for Compliance

Begin with wallet aggregation: import via API or CSV into a robust onchain PnL staking tracker. Tag staking deposits as non-taxable basis transfers, rewards as income at FMV via oracles like Chainlink. For disposals, apply your method consistently across assets; IRS proposals mandate FIFO absent election.

Document everything: screenshots of wallet states, transaction hashes linked to lot assignments. Multi-chain restakers, beware EigenLayer points or Symbiotic AVS yields; these morph into taxable drops. Quarterly reviews sync PnL with macro shifts, culling underwater lots preemptively.

Master DeFi Staking Taxes: FIFO/LIFO Guide for IRS Notice 2024-57 Compliance

Layer in stress tests: model 30% drawdowns or yield spikes. This foresight, honed over years tracking commodity cycles, reveals tax-efficient harvest windows. For instance, realize losses against high-basis staking income mid-year, offsetting DeFi staking rewards tax 2026 bites.

Consult professionals versed in Rev. Rul. 2019-24, affirming staking as income. As DeFi brokers emerge, hybrid reporting looms; until then, self-reliance rules. Tools like DefiTaxLots. com not only compute but educate, demystifying FIFO LIFO DeFi tax lots for enduring compliance.

Discipline today yields clarity tomorrow. In DeFi's relentless churn, measured tracking honors the patient investor, turning regulatory headwinds into tailwinds for sustained prosperity.

No comments yet. Be the first to share your thoughts!