2026 IRS Reporting Shift

The landscape of cryptocurrency taxation is shifting from a self-reporting model to one of mandatory, granular disclosure. Starting with the 2025 tax year, the IRS introduces Form 1099-DA, a new document designed to report gross proceeds from digital asset sales. While the initial phase focuses on transaction volume, the requirement for cost basis reporting begins phasing in during 2026, fundamentally changing how taxpayers must track their holdings [src-serp-2].

This transition demands wallet-level tracking. The IRS now requires taxpayers to track the cost basis of digital assets separately for each wallet or exchange used [src-serp-5]. For DeFi users who interact with multiple protocols and chains, this creates a complex data environment. Manual tracking is no longer a viable option; errors in lot selection can lead to significant overpayments or, worse, underreporting penalties during an audit.

Note: The 2025 filing season will see the first wave of 1099-DA forms. Ensure your tracking software is configured to handle wallet-level data before the 2026 cost basis mandates fully take effect.

The stakes are higher than ever. Incorrect lot tracking under these new rules can result in substantial tax liabilities. As major tax software providers update their documentation to reflect these changes, the burden of accuracy falls squarely on the taxpayer. Preparing your lot tracking strategy now is essential to managing the 2026 filing season with confidence.

FIFO, LIFO, and Specific ID: Which Cost Basis Method Fits Your Strategy?

Your choice of cost basis method is not just an accounting preference; it is a direct lever on your tax liability. Under the new guidance outlined in IRS Notice 2026-20, taxpayers now have explicit permission to select their own method—FIFO, LIFO, HIFO, or Specific ID—provided they apply it consistently and document the lots correctly.

The difference between these methods can be the difference between a substantial tax bill and a manageable one, especially in high-volatility DeFi environments. A single year of complex yield farming activity can generate hundreds of individual lots. Choosing the wrong method can lock you into paying taxes on gains that are already eroded by market downturns, or create an administrative nightmare that triggers an audit.

First-In, First-Out (FIFO)

FIFO is the default method for many jurisdictions and the most common choice for passive investors. Under FIFO, the first tokens you acquired are considered the first ones sold or swapped.

In a bull market, FIFO typically results in higher taxable gains because your earliest lots (acquired at lower prices) are sold first. In a bear market, it can be advantageous, as those low-cost early lots are gone, and you are left selling newer, higher-cost lots, potentially resulting in losses or smaller gains. FIFO is the simplest method to track, requiring no special identification at the time of sale, which makes it attractive for users with high transaction volumes who want to minimize record-keeping errors.

Last-In, First-Out (LIFO)

LIFO assumes that the most recently acquired tokens are the ones being sold or swapped first. This method has gained significant traction among active DeFi traders following the clarity provided in Notice 2026-20, which explicitly permits its use for cryptocurrency.

LIFO is often advantageous in rising markets. By selling your newest, highest-cost lots first, you reduce your taxable gain or increase your loss. This can significantly lower your immediate tax burden. However, LIFO requires meticulous tracking of your inventory. If you do not maintain precise records of every acquisition date and cost, you cannot reliably apply LIFO, and the IRS may default to FIFO, potentially resulting in a much larger tax bill.

Specific ID (Specific Lot Identification)

Specific ID allows you to designate exactly which lot of tokens you are selling at the time of the transaction. This offers the highest degree of control and tax optimization. If you hold multiple lots of the same token acquired at different prices and times, you can choose to sell the lot that results in the most favorable tax outcome for that specific transaction.

For example, if you need to harvest a loss, you can specifically identify the lot with the highest cost basis. If you want to defer taxes, you can choose to sell a lot with a low cost basis. The trade-off is complexity. Specific ID requires robust tracking software or detailed spreadsheets to link each sale to a specific acquisition lot. Without proper documentation, this method is risky and difficult to defend in an audit.

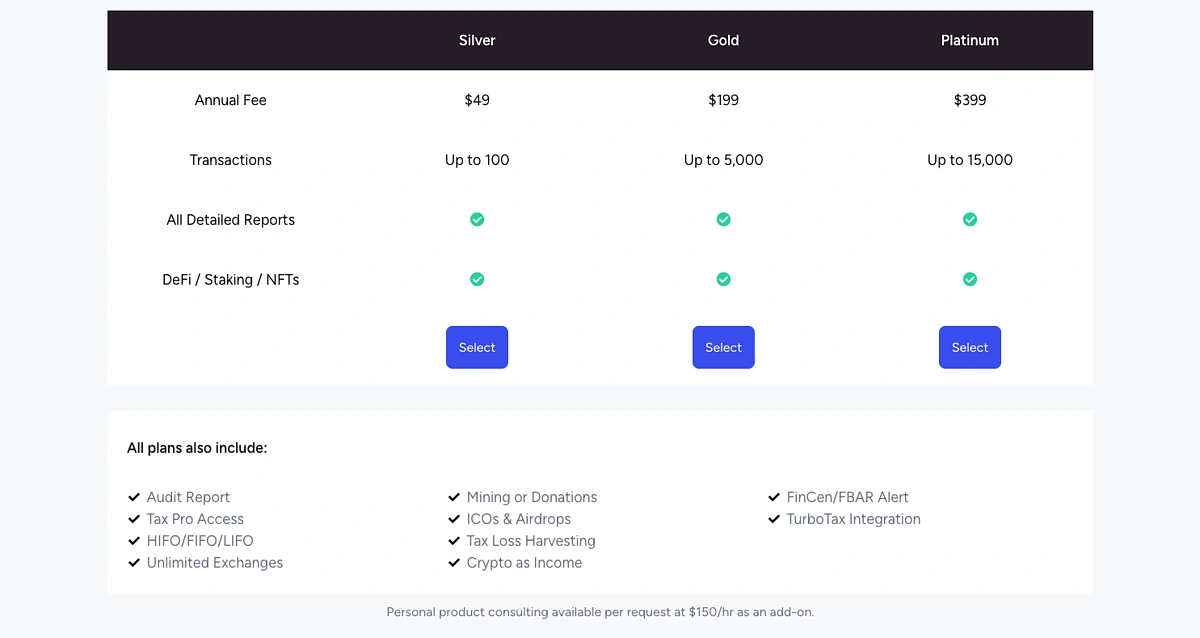

| Method | Tax Impact (Bull Market) | Tracking Complexity | Best For |

|---|---|---|---|

| FIFO | Higher gains (earliest lots sold) | Low | Passive investors & simple portfolios |

| LIFO | Lower gains (newest lots sold) | Medium-High | Active traders in rising markets |

| Specific ID | Customizable (optimized per trade) | High | Tax optimization & loss harvesting |

Yield Farming and Liquidity Pools

Providing liquidity to decentralized exchanges (DEXs) introduces a layer of tax complexity that standard exchange trading does not. When you deposit assets into a liquidity pool, you are not merely staking coins; you are exchanging them for liquidity provider (LP) tokens that represent your share of the pool. Under 2026 rules, this initial deposit often triggers a taxable event, as the IRS may view the conversion of distinct assets (e.g., ETH and USDC) into a single LP token as a disposition of the original assets. Getting the cost basis of the LP token right from day one is the foundation of accurate lot tracking.

The real risk emerges when you harvest rewards. Yield farming payouts—whether in the form of additional tokens or a share of trading fees—are treated as ordinary income at their fair market value on the date of receipt. Each time you claim these rewards, you establish a new cost basis for that specific amount. If you are using FIFO (First-In, First-Out) accounting, these newly acquired reward tokens sit at the front of the line when you eventually sell or swap them, potentially pushing more of your gains into higher short-term capital gains brackets.

Tracking these events requires precision because liquidity pools are dynamic. The ratio of assets in your pool changes constantly as traders interact with it. When you withdraw your liquidity, you are essentially redeeming your LP tokens for the underlying assets. This redemption is a taxable event where you must calculate the gain or loss on the LP tokens you are disposing of. Without automated lot tracking software that can reconcile on-chain data with IRS requirements, the margin for error is wide, and the financial penalties for underreporting can be severe.

The volatility inherent in DeFi tokens amplifies these risks. A sharp price swing in one of your paired assets can significantly alter the value of your position and the resulting tax liability. To visualize how price movements impact your lot valuation, consider the volatility seen in major DeFi governance tokens.

Software for Handling DeFi Complexity

The 2026 tax landscape demands precision that manual spreadsheets cannot provide. With the IRS treating hard fork proceeds as taxable income and enforcing strict lot identification rules, the margin for error has vanished. Incorrect lot tracking under FIFO or Specific ID methods can trigger unnecessary capital gains liabilities or audit flags. You need software that ingests on-chain data directly from your wallet and applies the correct accounting method automatically.

General-purpose tax tools often stumble when processing the high volume of transactions typical in DeFi. Automated lot tracking requires software that can distinguish between similar tokens across different liquidity pools and track cost basis through complex swaps. The right tool acts as a filter, separating reportable events from non-taxable internal transfers before they reach your final return.

Choosing the wrong platform risks costly corrections. Look for solutions that explicitly support DeFi protocols and provide clear audit trails. The cost of software is negligible compared to the potential penalties for misreported gains.

How Wash Sale Rules Apply to DeFi in 2026

The most significant advantage for DeFi investors in the 2026 tax landscape is the current absence of wash sale rules for digital assets. Unlike stock trades, where selling a security at a loss and repurchasing it within 30 days disallows the deduction, cryptocurrency transactions do not face this restriction. This gap allows investors to harvest losses without triggering a disallowed deduction, provided they follow the new cost basis reporting requirements correctly.

However, this advantage comes with high stakes. The IRS now mandates separate cost basis tracking for each wallet and exchange. If you sell a token at a loss to harvest it, then immediately buy it back in a different wallet, you must ensure your lot identification is precise. Incorrect lot tracking can lead to understated losses, resulting in unexpected tax bills or audits. The flexibility to harvest losses is only as valuable as the accuracy of your records.

This environment makes tax-loss harvesting a powerful but risky strategy. In volatile markets, the ability to offset gains with crypto losses can significantly reduce your overall tax burden. Yet, the complexity of tracking lots across multiple chains and wallets means that manual tracking is prone to error. Using specialized tax software that integrates with DeFi protocols is no longer optional; it is essential for compliance.

While the lack of wash sale rules offers flexibility, it does not eliminate the need for careful planning. Each sale and repurchase must be documented clearly to withstand potential IRS scrutiny. The financial risk of incorrect lot tracking under these new rules is substantial, making precision in your DeFi tax lot tracking the single most important factor in optimizing your 2026 tax outcome.

Prepare Your 2026 Tax Strategy

The 2026 tax season introduces strict cost-basis tracking requirements that make manual record-keeping nearly impossible. The IRS now requires taxpayers to track the cost basis of digital assets separately for each wallet or exchange. If you cannot prove the acquisition date and cost of every unit sold, the IRS may assume the worst-case scenario: that all gains are short-term or that no cost basis exists at all. This can lead to significant overpayment or severe penalties.

To avoid this, you must treat your tax preparation as a continuous process rather than an end-of-year scramble. Follow these steps to organize your data and select the right cost-basis method before the filing deadline.

Use a reputable tax software provider to import transaction history from every wallet and exchange you used in 2025. Ensure all DeFi interactions, including staking rewards and liquidity pool deposits, are captured. Missing a single exchange can result in unreported income, which triggers audits.

Choose between FIFO (First-In, First-Out), LIFO (Last-In, First-Out), or Specific Identification. FIFO is the default for most platforms but may not minimize taxes if prices are rising. Specific Identification allows you to pick exactly which tokens you sold, offering the most control but requiring meticulous record-keeping. Consult IRS Publication 544 for detailed rules on cost basis methods.

Liquidity pool positions and staking rewards are taxable events. Ensure your software correctly identifies the fair market value of tokens received at the time of receipt. Incorrect valuation of these rewards can lead to underreporting income, a common audit trigger.

Given the complexity of 2026 rules, engage a CPA or tax attorney who specializes in digital assets. They can help you interpret new guidance, identify deductions, and ensure your chosen cost-basis method is applied consistently. Early engagement prevents last-minute errors and potential penalties.

No comments yet. Be the first to share your thoughts!