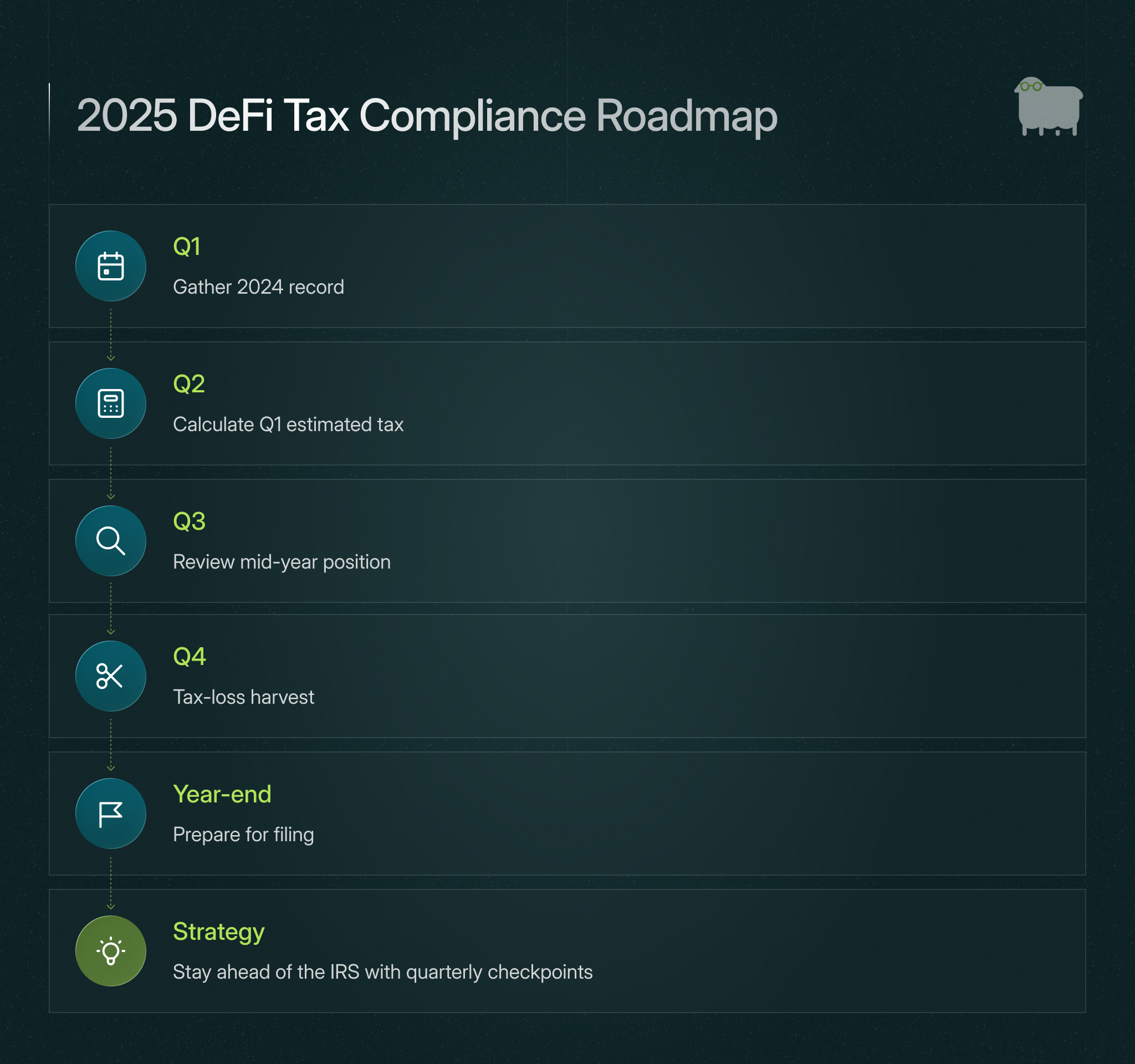

Track DeFi tax lots 2026 from the start

The 2026 tax season introduces a fundamental shift in how digital assets are reported. Under the new IRS Form 1099-DA rules, cost basis reporting for digital asset transactions becomes mandatory. This requirement applies to all crypto transactions, including those occurring in decentralized finance (DeFi) protocols. The goal is to provide the IRS with a clear, standardized record of gains and losses, reducing the reliance on self-reported data alone.

For DeFi users, the challenge is particularly acute. Liquidity provider tokens and liquid staking tokens (LSTs) often lack the straightforward acquisition records of simple spot purchases. Tracking these assets requires meticulous attention to the exact moment of receipt, the value at that time, and any subsequent staking rewards or yield distributions. Failure to track these tax lots accurately can lead to significant discrepancies when the new 1099-DA forms are issued.

Start tracking your DeFi tax lots immediately. Do not wait for the end of the year to reconcile your wallet activity. The complexity of DeFi transactions means that historical data can be difficult to retrieve or interpret retroactively. By establishing a consistent tracking method now, you avoid the risk of missing critical data points that will be required for accurate cost basis calculation under the new regulations.

Calculate cost basis for liquid staking tokens

Determining the correct cost basis for liquid staking tokens (LSTs) like stETH or rETH requires tracking two distinct events: the initial acquisition and the subsequent receipt of staking rewards. Under current IRS guidance, these events trigger separate tax liabilities. The initial purchase establishes your cost basis, while the staking yield is treated as ordinary income at the moment you gain dominion and control over the rewards.

Follow this sequence to calculate your DeFi tax lots accurately for the 2026 tax year.

When you swap ETH for an LST on a decentralized exchange or centralized platform, you have disposed of the original ETH and acquired a new asset. Record the value of the LST at the exact time of the swap. This value becomes your initial cost basis. If you used ETH that was previously purchased, you must also calculate the gain or loss on the original ETH disposal using your chosen accounting method (FIFO, LIFO, or Specific Identification).

Liquid staking protocols distribute rewards periodically, often automatically compounding into your balance. Each time the protocol credits rewards to your wallet or increases your LST balance, you must capture the value of the reward tokens at that specific moment. This value is your taxable ordinary income for that tax year. Do not wait until you sell the LST to report this income; the event occurs when the reward is claimable or automatically compounded.

Your total cost basis in the LST position increases by the amount of income you reported for each reward event. For example, if you bought 10 stETH for $3,000 and later received $100 worth of stETH rewards (which you reported as income), your new total cost basis is $3,100. This adjusted basis is critical for calculating capital gains or losses when you eventually sell or swap the LSTs.

Maintain a detailed ledger for every LST transaction. This includes the timestamp of the initial swap, the timestamp of each reward distribution, and the USD value of the LST at both moments. IRS regulations require precise records to substantiate your cost basis calculations. Use tax software that supports DeFi transaction tracking to automate this aggregation from multiple wallets and protocols.

Failure to separate the initial cost basis from the income basis of rewards can lead to underreporting income or overreporting capital gains. By treating the initial acquisition and the reward accrual as distinct events, you ensure your 2026 calculations align with IRS digital asset guidance.

Recognize staking rewards as taxable income

The IRS treats staking rewards as ordinary income, but the timing of that recognition depends on one specific factor: dominion and control. You do not owe tax the moment a protocol credits your wallet with new tokens. You owe tax when you actually gain the ability to use, transfer, or dispose of those rewards.

This standard comes directly from IRS Notice 2014-21, which defines virtual currency as property subject to federal tax rules. The notice states that staking rewards are includible in gross income in the taxable year in which the taxpayer gains "dominion and control" over the rewards. This means the tax event is tied to your actual access, not the protocol's internal accounting.

For 2026, this distinction is critical for accurate reporting. If your rewards are locked in a smart contract or require a specific transaction to claim, your income is not recognized until you execute that claim or the lock expires. Once you have dominion and control, the value of the tokens at that exact moment becomes your cost basis.

This new cost basis sets the foundation for all future transactions involving those specific tokens. When you eventually sell or swap them, your gain or loss is calculated against this initial income value. Misidentifying the moment of dominion and control can lead to underreporting income or using an incorrect cost basis, both of which create significant errors in your 2026 records.

Match lots when you unstake or swap

When you redeem liquid staking tokens (LSTs) or swap them on a decentralized exchange, you trigger a taxable event. You must match the specific tokens leaving your wallet to the original purchase lots to calculate the correct capital gain or loss. This process is the core of managing your 2026 tracking, especially under the new IRS Form 1099-DA reporting requirements.

You can choose between specific identification or First-In, First-Out (FIFO) methods. Specific identification lets you pick which lot to dispose of, which is useful for tax planning if you hold lots with different entry prices. FIFO automatically sells your oldest holdings first. Under the 2026 rules, you must maintain clear records to support your chosen method, as the IRS expects wallet-level tracking to align with your reported gains.

To calculate the gain, subtract the cost basis of the matched lot from the value of the LST at the time of the transaction. If you hold the tokens for more than one year, you may qualify for long-term capital gains rates. Keep detailed logs of every unstake and swap to ensure your 2026 records are accurate and defensible.

Avoid common LST tracking mistakes

Most 2026 errors stem from treating staking rewards as simple income events rather than distinct cost basis updates. If you ignore the value at the moment rewards are credited, your capital gains calculations will be wrong. This is the most frequent error in LST reporting.

Another critical mistake is failing to update your cost basis after staking events. When you restake or compound rewards, the original asset's basis changes. You must track each micro-event to ensure your cost basis reflects the true average purchase price. Ignoring these adjustments leads to over-reported gains and unnecessary tax liability.

Finally, remember that DeFi gains are not invisible. The IRS is using advanced blockchain analytics to track "hidden" wallets. Assuming anonymity protects you from reporting requirements is a dangerous gamble. Keep your records precise and current to avoid audits.

Defi tax lots 2026: frequently asked: what to check next

Understanding how the IRS treats liquid staking derivatives (LSDs) and LSTs requires tracking two distinct taxable events: receipt of rewards and disposal of assets. The following questions address the most common compliance hurdles for 2026.

Always verify lot calculations against your exchange records before filing. The 2026 reporting landscape demands precise tracking of every deposit, reward claim, and swap.

No comments yet. Be the first to share your thoughts!